You swear, starting today, you’re going to curb your spending. And you really mean it. Until….

You spy an online ad for this adorable summer dress that’s to die for. Later, you flip through the Costco catalogue and that Vitamix Blender you’ve been eyeing is on sale.

Without thinking, you whip out your card, make your purchase and you feel great. Until the bill comes. Then you remember your vow and beat yourself up for not having more will-power.

BUT WAIT! According to the latest research, all the will power in the world may not be enough. Blame it on your brain.

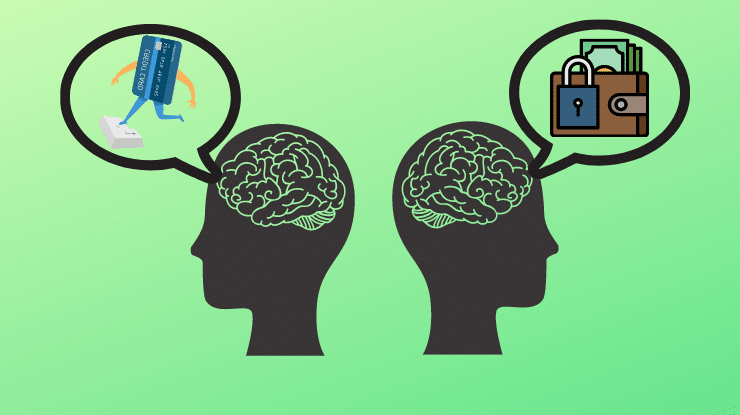

A recent study did brain scans on people who planned to buy with credit cards and those planning to use cash. They discovered a notable disparity in brain activity between the two groups.

“Buying on credit doesn’t just ease shoppers’ inhibitions,” reports the Wall Street Journal. “It actively encourages purchases.”